Yield Report: Interest Rate Commentary (29 July – 2 August 2024)

The FOMC meeting concluded on Wednesday night (AEDT) with the decision to maintain the federal funds target range at 5.25% to 5.50%. The official statement saw minor adjustments, notably the line, "...there has been some further progress toward the Committee’s 2% inflation objective." This led cash futures markets to anticipate a September rate cut, with prices reflecting a high level of certainty for such a move.

In related news, a debate among economists emerged over whether the "Sahm Rule" was triggered by the latest non-farm payrolls data released on Friday. The rule, often used as a recession indicator similar to an inverted yield curve, saw contention over whether the calculation should be to one or two decimal places. According to the St. Louis Fed, the conditions for recession as per the Sahm Rule were met, which led to a flight to safety in US markets on Friday, with share prices dropping and US Treasury yields plummeting.

Sovereign 10-year bond yields ended the week lower across Australia, the US, and major European markets. Yield curves steepened in Australia and became less negative or more positive in the US.

In the domestic cash market, cash futures prices, which closely track the actual cash rate, indicated a substantially lower trajectory for the cash rate through the 2023/24 financial year. Expectations of short-term rate hikes have now dissipated.

There were a few changes to term deposit rates this week, with the highest available rate in the survey declining to 5.10%.

The 3-month BBSW saw a noticeable drop. Historically, the 3-month BBSW has held a modest premium (15bps) over the cash rate, but the premium narrowed to 7bps by the end of the week.

The median margin of ASX-listed hybrids finished slightly lower, falling below the lower bound of the range that captures most median margin readings since 2011, yet remaining just above its series low.

Swap rates generally declined more sharply than Australian Commonwealth Government Bonds (ACGBs).

Risk measures in corporate bonds, such as swap spreads, tightened, while credit default swap premiums remained relatively stable on average.

The ICE Bank of America BBB US Corporate Index Option-Adjusted spread increased by 6bps to 1.23%. Typically, the spread ranges between 1.00% and 3.00% in "normal" years.

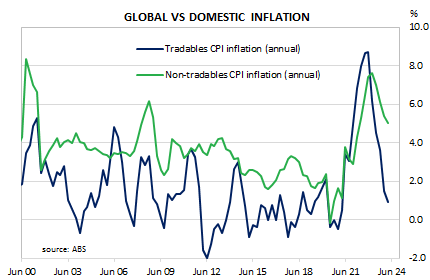

Chart of the Week

Excess demand for haircuts continues...

| Name | Week Close | Week Change | Week High | Week Low |

|---|---|---|---|---|

| Cash Rate% | 4.35 | |||

| 3m BBSW % | 4.41 | -0.08 | 4.49 | 4.41 |

| Aust 3y Bond %* | 3.64 | -0.31 | 3.98 | 3.59 |

| Aust 10y Bond %* | 4.06 | -0.26 | 4.34 | 3.99 |

| Aust 20y Bond %* | 4.46 | -0.21 | 4.64 | 4.42 |

| US 2y Bond % | 3.88 | -0.50 | 4.40 | 3.88 |

| US 10y Bond % | 3.79 | -0.41 | 4.17 | 3.79 |

| US 30y Bond % | 4.11 | -0.34 | 4.43 | 4.11 |

| iTraxx | 66.00 | 0.00 | 66.00 | 65.00 |

| $1AUD/US¢ | 65.11 | -0.35 | 65.68 | 64.80 |

"Finexia Financial Expands into Fixed Income with Yield Report Acquisition | ASX Update")

"Response to Media Speculation")

"Notice of Annual General Meeting 2025")

"Finexia Annual Report 2025")

"Leadership Transition and Strengthening of Core Functions")

"Confirmation of Release - FNX - Proposed Transaction and Market Update")

"Resignation of Interim CEO")